New vs. Old Tax Regimes for AY 2024-25: Which is better?

A Comprehensive Guide to New vs Old Tax Regimes for AY 2024-25

Introduction: Understanding the Tax Regimes

With the introduction of the new tax regime in 2020, many taxpayers in India now have a choice between two filing options for AY 2024-25. The case wasn't always that strong for the New Regime, however the Budget 2023 has really upped the game for the individuals to opt for it now.

For the unaware, the GOI had introduced a scheme of Income tax in India in the Union Budget 2020-21 mostly prompted by the notion that the millennial generation is exhibiting a proactivity towards spending rather than saving. This scheme aims to simplify the filing process by offering lower tax rates and eliminating most deductions. This regime is designed to be more user-friendly, particularly for those who don't have extensive tax-saving investments or deductions.

The expectation till FY 2022-23 was the changes in tax brackets would occur in a gradual rather than sudden manner. But despite the simplified mechanism and reduced tax burden of the New Tax Regime, taxpayers were still choosing to opt for the old regime and took advantage of tax deductions. Hence the latest changes were presented in the Union Budget 2023-24 which brought significant changes in the earlier existing policy.

Let’s look at both regimes and see which regime to opt for in 2024.

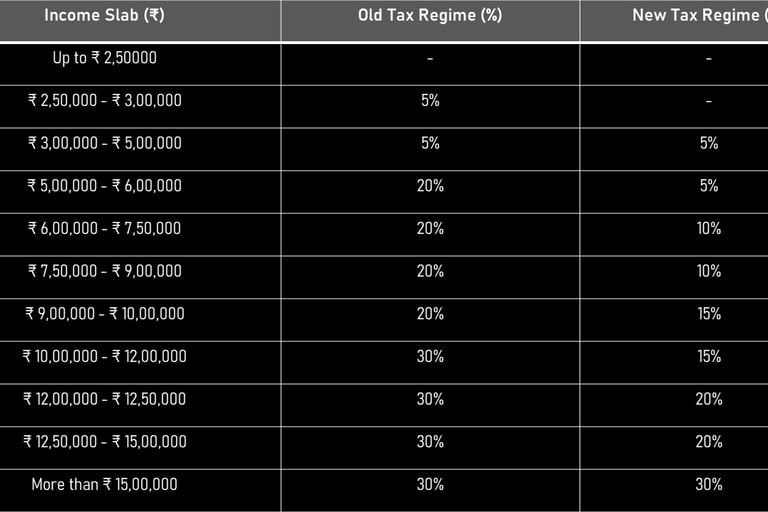

Slab Rate Comparison: New vs. Old Regime

Here's a table outlining the income tax slab rates for AY 2024-25 under both regimes:

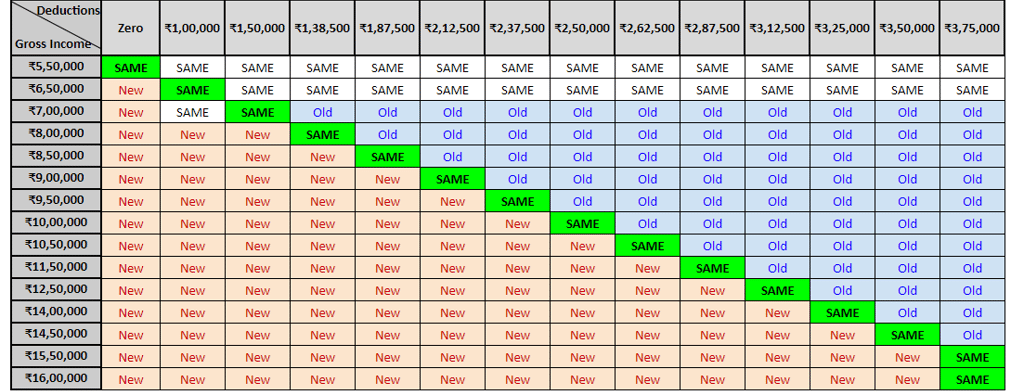

Understanding the difference : A Real-world example

Let's consider Mr. Shah, a salaried individual with an annual income of ₹12.53 lakh. He has investments in ELSS mutual funds for ₹ 1.2 lakh and pays health insurance premiums for himself and his parents for ₹ 0.18 lakh.

Old Tax Regime : In this regime, Mr. Shah can claim deductions under various sections like 80C, 80D, and others, potentially reducing his taxable income and tax liability. According to above rates, the income tax payable will be ₹ 1,37,280 on Net Taxable Income of ₹ 10.65 lakhs.

New Tax Regime : This regime offers lower tax rates but eliminates most deductions, including those mentioned above. In this regime the income tax payable will be ₹ 94,224 on Net Taxable Income of ₹ 12.03 lakhs.

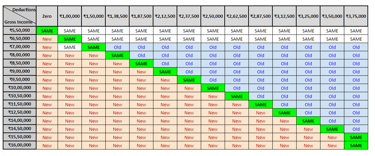

The decision to make out the better regime for you depends on various factors such as your income level, type of income, eligibility for deductions, personal goals, long-term plannings, etc. Here is a breakeven point chart for salaried individuals under 60 years of age :

Compare your income tax liability under both schemes here.

Deductions allowed in the New Tax Regime

Below mentioned deductions and exemptions are allowed in the New Tax Regime along with the Old Tax Regime :

Standard Deduction of ₹ 50,000.

Rebate u/s 87A for ₹25,000 (Under Old Scheme, it is limited up to ₹ 12,500)

Perks for official purposes

Interest of Home loan for Let out properties

Employer's NPS contribution

Contributions to Agniveer Corpus Fund

Family Pension deduction

Gifts up to ₹ 50,000

VRS (Voluntary Retirement Scheme)

Gratuity

Leave Encashment

Daily Allowance

Conveyance Allowance

Transport Allowance for a specially abled person

Deductions disallowed in the New Tax Regime

Below mentioned deductions and exemptions are disallowed in the New Tax Regime :

House Rent Allowance (HRA)

Leave Travel Allowance (LTA)

Any other Allowances

Entertainment allowance

Professional Tax

Interest on Home Loan for Self Occupied or vacant property

Deductions u/s 80C such as EPF, LIC, ELSS, PPF, FD, Tuition Fee, etc

Employee's contribution to NPS

Medical Insurance premium

Disabled Individual deduction

Interest on Educational Loan

Interest on EV Loan

Donation to Political Party / Trust, etc.

Savings Banks Interest

Other Chapter VI-A deductions

Conclusion

Many individuals often find themselves questioning the disparities between the old and new tax regimes. The new income tax regime is designed to accommodate those who have more personal commitments such as repayment of personal/vehicle loans, medical treatment of parents or dependents, or wish to avoid the burden of extensive tax preparation or have minimal tax deductions due to their ineligibility for section 10 exemptions, standard deductions, tax on employment, employer contribution to pension scheme etc., Conversely, the old tax regime can yield more tax savings for senior citizens, who derive a substantial portion of their income from interest, can benefit from Section 80TTB, which allows them to claim Rs.50,000 as interest income deduction and feel more secure under the old tax regime.

Both the old and new tax regimes possess advantages and disadvantages. The previous tax structure encourages taxpayers to cultivate a habit of saving, while the new tax structure favors employees with lower earnings and investments, resulting in fewer deductions and exemptions. The new tax system is considered safer and simpler, involving fewer records and reducing the potential for tax evasion fraud. However, due to the unique nature of individual deductions and exemptions, a thorough comparison of the two regimes is necessary to determine the best fit for each person.

Let's conquer the world of Taxes together, one step at a time! You can reach out to the Numbreylla Team for any assistance.