Pricing Strategies for your business

A blog on developing a Pricing Strategy to maximize profit without scaring customers away

Creating an effective pricing strategy is one of the most critical decisions for any business. Price too high, and you risk alienating customers; price too low, and you could end up eroding your profit margins. A well-crafted pricing strategy serves as a crucial tool for achieving key objectives, primarily maximizing profit while ensuring the business remains competitive.

Below, we’ll take a deep dive into how you can develop a pricing strategy that maximizes profit while keeping your customers happy and loyal.

Understanding the Core principles

A pricing strategy is much more than slapping a price tag on your product or service. It’s a deliberate approach that takes into account several factors:

Cost of Goods Sold (COGS): This includes all expenses directly tied to producing or delivering a product or service.

Market Demand: How much are your customers willing to pay for your offerings?

Competition: What are your competitors charging for similar products or services?

Value Proposition: What unique value are you providing that justifies your price?

Profit Margin: The percentage of the final sale price that exceeds the cost of production, contributing directly to profit.

Each of these factors needs to be carefully balanced to achieve optimal pricing.

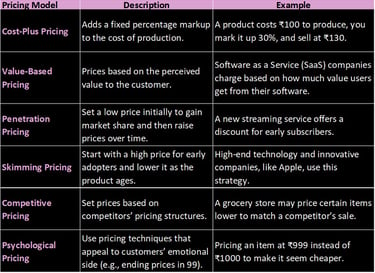

Popular Pricing Models

Before crafting your strategy, it’s important to know the various pricing models that businesses commonly use:

Choosing the right model depends on your industry, target audience, and the product lifecycle.

Steps to Develop a Profitable Pricing Strategy

Step 1: Analyze Costs

Your baseline for any pricing decision is the total cost of production (or service delivery). This includes:

Fixed Costs: Rent, salaries, insurance, etc.

Variable Costs: Materials, shipping, hourly labor.

Hidden Costs: Warranty claims, returns, after-sales support.

Using the formula:

Price=COGS+ Desired Profit

you can estimate a minimum viable price. Ensure you're covering costs without setting a price too low to maintain sustainability.

Step 2: Understand Your Customers’ Willingness to Pay

Conducting market research to identify how much your customers value your product or service is crucial. This can be done via:

Surveys

Focus groups

Competitor analysis

Sometimes, testing different price points through A/B testing on a small subset of customers can give you valuable data.

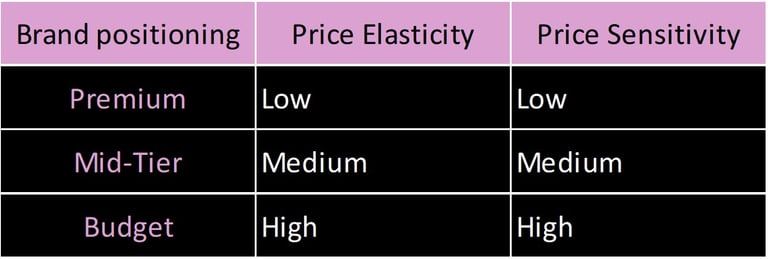

Step 3: Evaluate Market Positioning

Is your brand premium, mid-tier, or budget? Your positioning will determine how price-sensitive your customers are. For example:

Premium brands can charge more if they deliver superior quality and exclusivity.

Mid-tier brands need to provide a balanced value proposition—good quality for reasonable prices.

Budget brands focus on low prices and high sales volumes.

Understanding where your business fits in this table helps align your pricing strategy with your market.

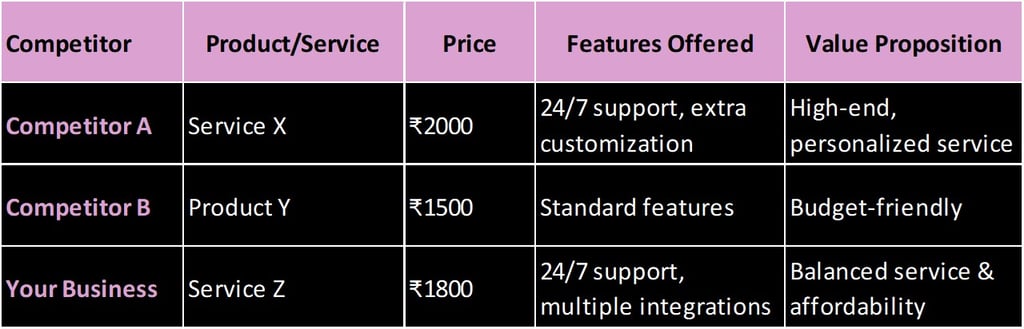

Step 4: Competitive Analysis

Knowing what your competitors are charging helps you avoid two major pitfalls:

Overpricing: This may lead to losing price-sensitive customers.

Underpricing: This may devalue your product and squeeze your profit margins.

Create a competitive pricing table to understand where you stand in comparison:

Pricing Tactics to Avoid Alienating Customers

Transparency

Customers appreciate honest pricing. If you must charge extra for add-ons or features, make sure those costs are communicated upfront. Hidden fees frustrate customers and damage trust.

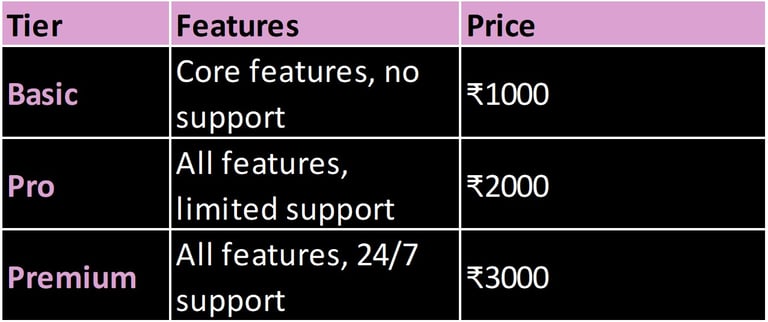

Tiered Pricing

Offering multiple price points for different customer segments is a powerful strategy. For instance:

This allows price-sensitive customers to opt for the lower tier while maximizing revenue from customers who are willing to pay for premium features.

Psychological Pricing

Studies show that ending prices with .99, .95, or other non-round numbers can make prices seem significantly lower to consumers. A product priced at ₹1999 feels much cheaper than ₹2000, despite the small difference.

Discounts & Promotions

Using limited-time discounts can drive urgency and help capture price-sensitive customers without permanently lowering your prices. However, avoid excessive promotions that train customers to expect discounts.

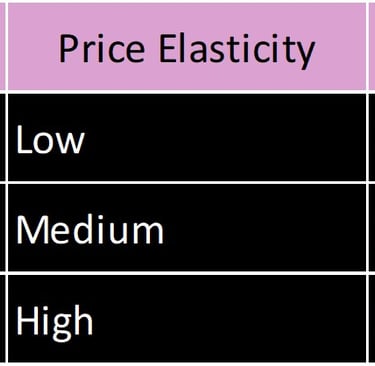

Tracking and Adjusting Your Pricing Strategy Over Time

Once you've launched a pricing strategy, the work doesn't stop. Regularly monitor key metrics like:

Customer Acquisition Cost (CAC)

Customer Lifetime Value (CLV)

Profit Margins

Price Elasticity

You should be prepared to adapt your pricing as your business grows or market conditions change. For instance, in response to increased competition, you may need to revisit your value proposition or introduce new pricing tiers to stay competitive.

Conclusion

Developing a pricing strategy that maximizes profit without alienating customers is both an art and a science. It requires a deep understanding of your costs, customer behavior, market dynamics, and competitive landscape. By using the techniques outlined in this blog—analyzing costs, leveraging different pricing models, studying competitors, and applying psychological pricing—you can craft a strategy that ensures profitability while maintaining customer satisfaction.

Remember, the key to a successful pricing strategy is flexibility and regular evaluation. Pricing is not a "set it and forget it" task; it requires continuous refinement as your business and the market evolve.

By following these steps and constantly adapting to changes, you can avoid pricing pitfalls and drive long-term profitability without scaring away your customers.

Creating an effective pricing strategy is one of the most critical decisions for any business. Price too high, and you risk alienating customers; price too low, and you could end up eroding your profit margins. A well-crafted pricing strategy serves as a crucial tool for achieving key objectives, primarily maximizing profit while ensuring the business remains competitive.

Below, we’ll take a deep dive into how you can develop a pricing strategy that maximizes profit while keeping your customers happy and loyal.

Understanding the Core principles

A pricing strategy is much more than slapping a price tag on your product or service. It’s a deliberate approach that takes into account several factors:

Cost of Goods Sold (COGS): This includes all expenses directly tied to producing or delivering a product or service.

Market Demand: How much are your customers willing to pay for your offerings?

Competition: What are your competitors charging for similar products or services?

Value Proposition: What unique value are you providing that justifies your price?

Profit Margin: The percentage of the final sale price that exceeds the cost of production, contributing directly to profit.

Each of these factors needs to be carefully balanced to achieve optimal pricing.

Popular Pricing Models

Before crafting your strategy, it’s important to know the various pricing models that businesses commonly use:

Choosing the right model depends on your industry, target audience, and the product lifecycle.

Steps to Develop a Profitable Pricing Strategy

Step 1: Analyze Costs

Your baseline for any pricing decision is the total cost of production (or service delivery). This includes:

Fixed Costs: Rent, salaries, insurance, etc.

Variable Costs: Materials, shipping, hourly labor.

Hidden Costs: Warranty claims, returns, after-sales support.

Using the formula:

Price=COGS+ Desired Profit

you can estimate a minimum viable price. Ensure you're covering costs without setting a price too low to maintain sustainability.

Step 2: Understand Your Customers’ Willingness to Pay

Conducting market research to identify how much your customers value your product or service is crucial. This can be done via:

Surveys

Focus groups

Competitor analysis

Sometimes, testing different price points through A/B testing on a small subset of customers can give you valuable data.

Step 3: Evaluate Market Positioning

Is your brand premium, mid-tier, or budget? Your positioning will determine how price-sensitive your customers are. For example:

Premium brands can charge more if they deliver superior quality and exclusivity.

Mid-tier brands need to provide a balanced value proposition—good quality for reasonable prices.

Budget brands focus on low prices and high sales volumes.

Understanding where your business fits in this table helps align your pricing strategy with your market.

Step 4: Competitive Analysis

Knowing what your competitors are charging helps you avoid two major pitfalls:

Overpricing: This may lead to losing price-sensitive customers.

Underpricing: This may devalue your product and squeeze your profit margins.

Create a competitive pricing table to understand where you stand in comparison:

Pricing Tactics to Avoid Alienating Customers

Transparency

Customers appreciate honest pricing. If you must charge extra for add-ons or features, make sure those costs are communicated upfront. Hidden fees frustrate customers and damage trust.

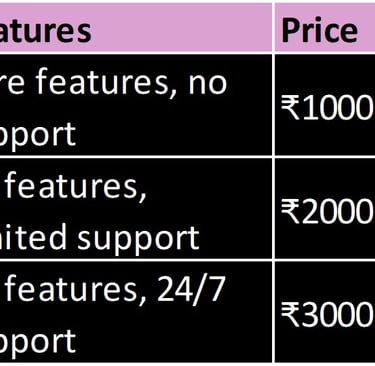

Tiered Pricing

Offering multiple price points for different customer segments is a powerful strategy. For instance:

This allows price-sensitive customers to opt for the lower tier while maximizing revenue from customers who are willing to pay for premium features.

Psychological Pricing

Studies show that ending prices with .99, .95, or other non-round numbers can make prices seem significantly lower to consumers. A product priced at ₹1999 feels much cheaper than ₹2000, despite the small difference.

Discounts & Promotions

Using limited-time discounts can drive urgency and help capture price-sensitive customers without permanently lowering your prices. However, avoid excessive promotions that train customers to expect discounts.

Tracking and Adjusting Your Pricing Strategy Over Time

Once you've launched a pricing strategy, the work doesn't stop. Regularly monitor key metrics like:

Customer Acquisition Cost (CAC)

Customer Lifetime Value (CLV)

Profit Margins

Price Elasticity

You should be prepared to adapt your pricing as your business grows or market conditions change. For instance, in response to increased competition, you may need to revisit your value proposition or introduce new pricing tiers to stay competitive.

Conclusion

Developing a pricing strategy that maximizes profit without alienating customers is both an art and a science. It requires a deep understanding of your costs, customer behavior, market dynamics, and competitive landscape. By using the techniques outlined in this blog—analyzing costs, leveraging different pricing models, studying competitors, and applying psychological pricing—you can craft a strategy that ensures profitability while maintaining customer satisfaction.

Remember, the key to a successful pricing strategy is flexibility and regular evaluation. Pricing is not a "set it and forget it" task; it requires continuous refinement as your business and the market evolve.

By following these steps and constantly adapting to changes, you can avoid pricing pitfalls and drive long-term profitability without scaring away your customers.