Tax Deductions for Capital Gains

A detailed guide towards understanding the deductions available against Capital Gain income

Overview of Capital Gains and Tax Deductions

Are you looking for ways to reduce your tax liability?

If so, you may be able to take advantage of the capital gains tax deductions available under the Income Tax Act. Budget 2024 has brought some serious changes for Capital Gain Taxes ranging from holding periods and tax rates to indexation benefits removal, and now, reintroduction as an option.

Capital gains represent the profit earned from the sale of an asset, such as real estate, stocks, or bonds, when the selling price exceeds the purchase price. These gains are classified into two categories: short-term capital gains (STCG) and long-term capital gains (LTCG), each subject to different tax treatments under Indian tax laws.

Short-term capital gains arise when an asset is held for a brief period—typically less than 12 or 24 months (36 months holding period now removed). These gains are typically taxed at a higher rate than the Long-term capital gains.

Tax deductions and exemptions play a crucial role in the financial planning of individuals and investors. These mechanisms are instituted to incentivize particular types of investments or economic activities, thereby promoting growth and financial stability. For instance, Section 80C offers deductions on specific investment instruments, while Section 10 offers exemptions on certain types of incomes.

Among the most significant provisions for tax relief on capital gains are Sections 54 and its related sections of the Income Tax Act. These sections primarily address exemptions on long-term capital gains, particularly from the sale of residential property, provided the gain is reinvested in specified assets, such as another residential property. This legal framework not only helps taxpayers significantly reduce their overall tax liability but also encourages the reinvestment of gains into the real estate market, bolstering economic activity within this sector.

Detailed Explanation of Section 54 and Its related sections

Section 54 and its related sections of the Income Tax Act provides avenues for taxpayers in India to reduce their capital gain tax liability through reinvestment. Here is a comprehensive breakdown of all those provisions, designed for easy understanding.

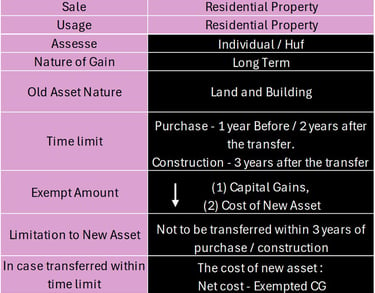

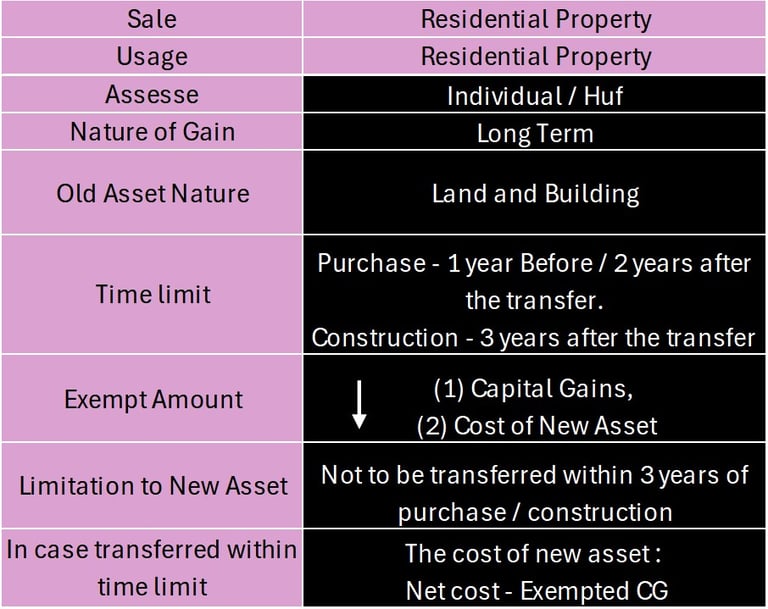

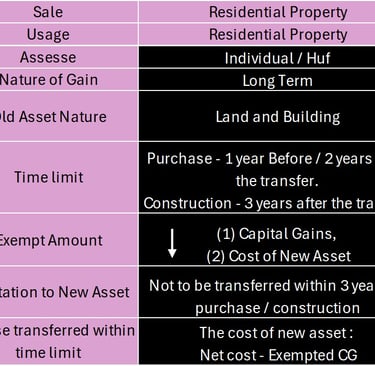

Section 54

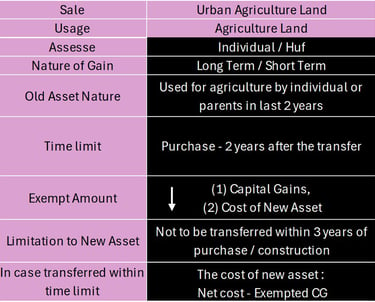

Section 54B

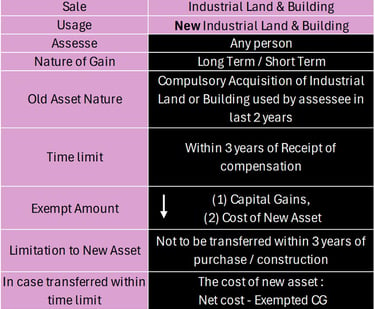

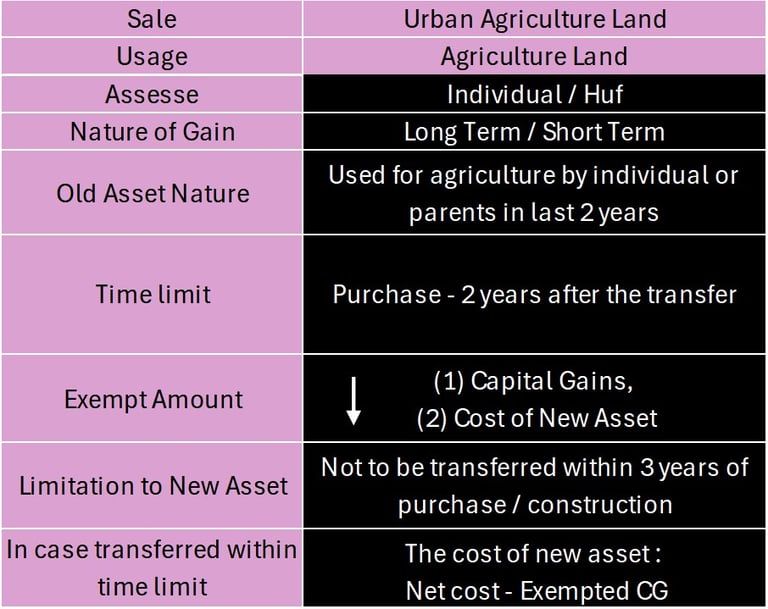

Section 54D

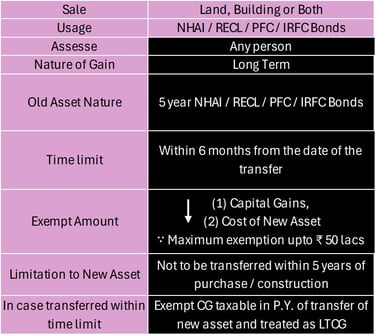

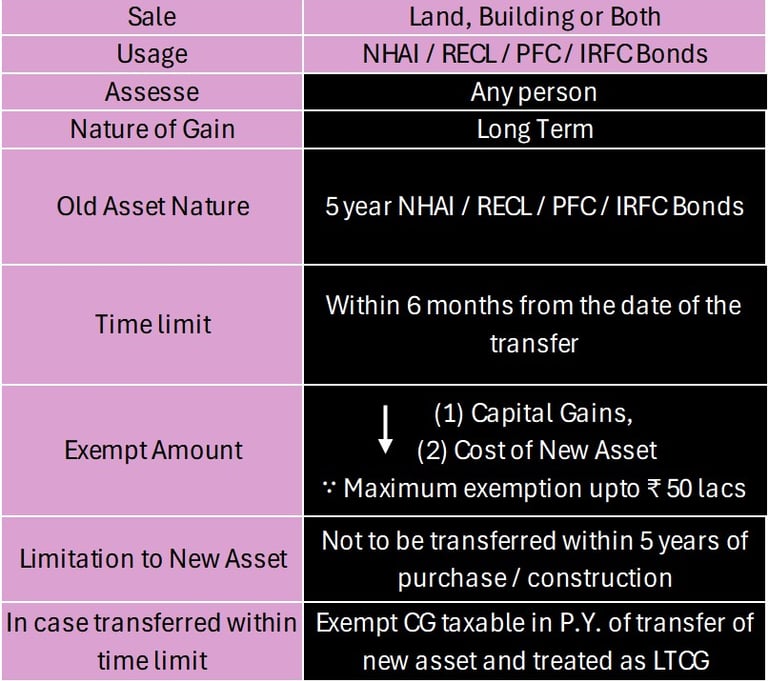

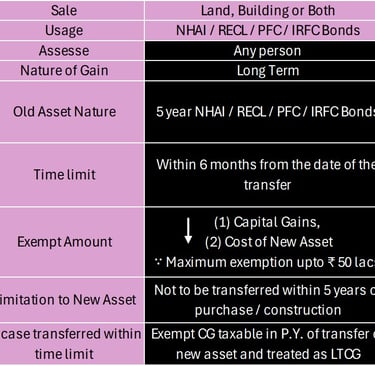

Section 54EC

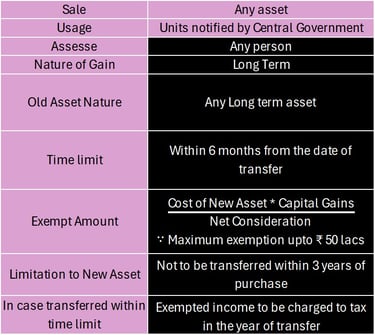

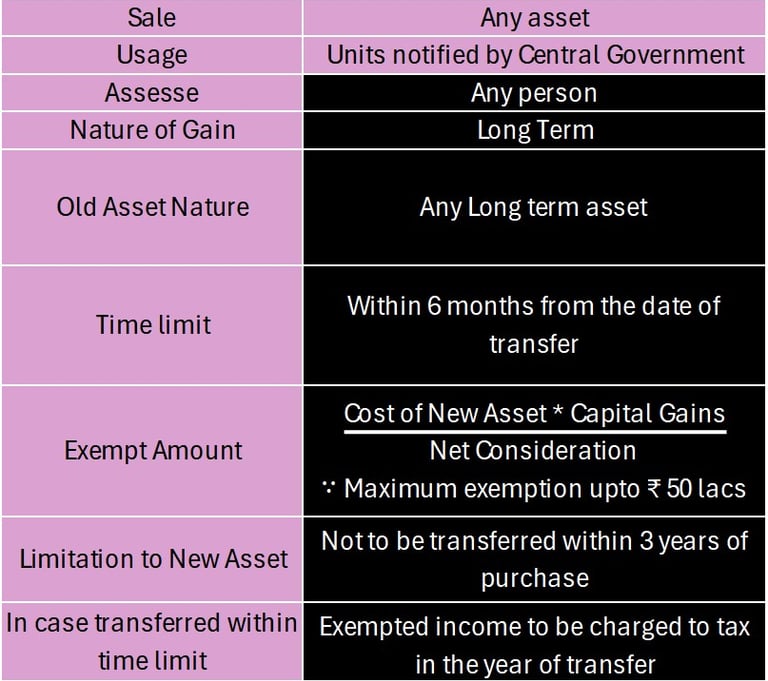

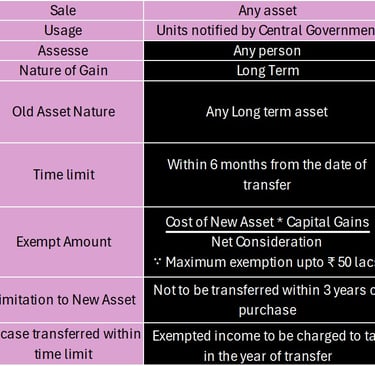

Section 54EE

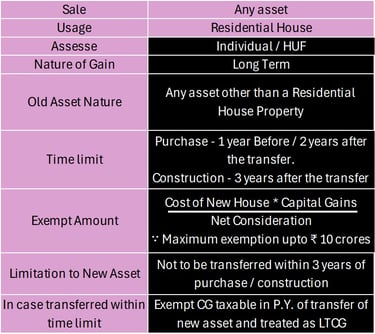

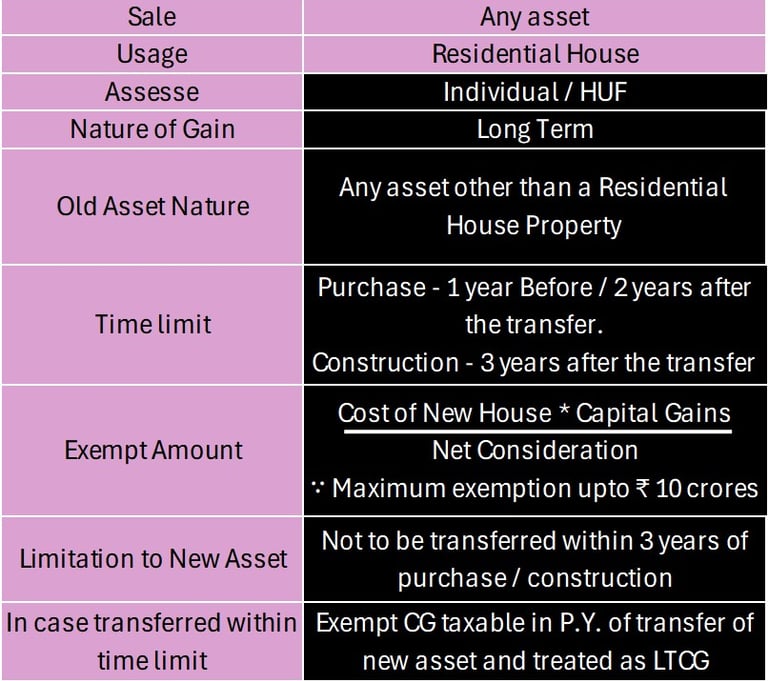

Section 54F

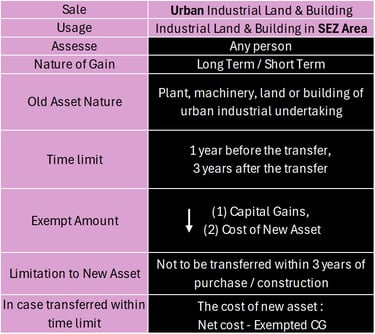

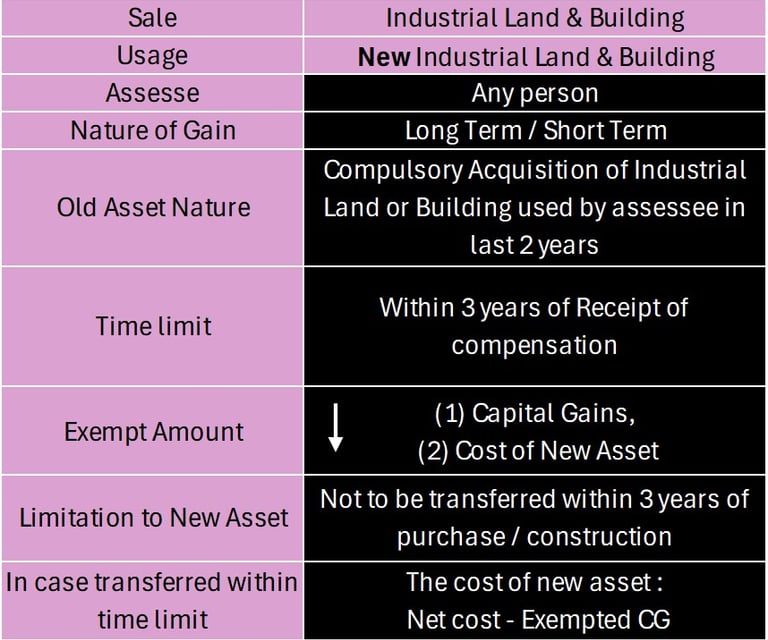

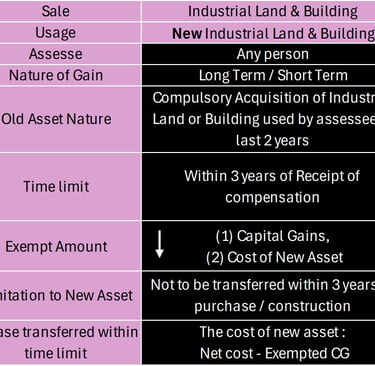

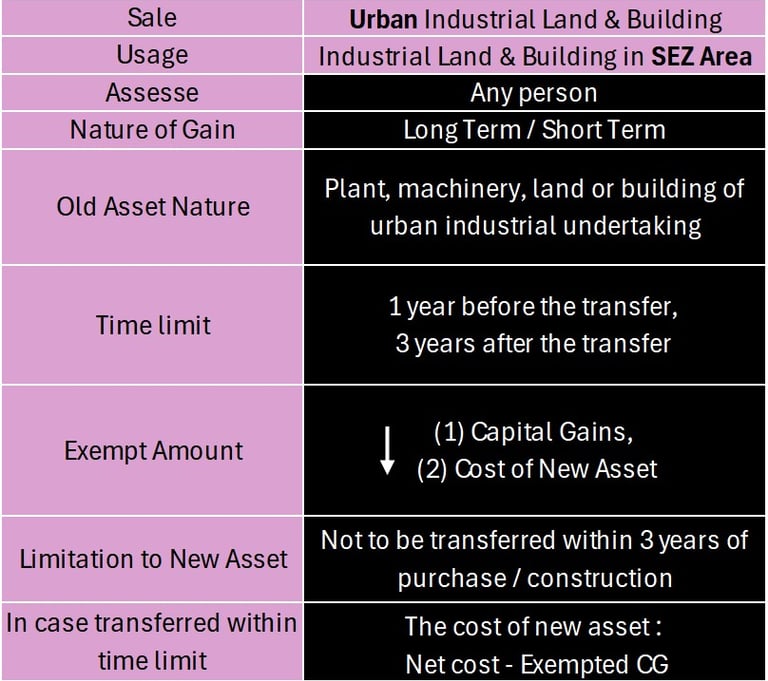

Section 54G

Section 54GA

Some Points to note :

Capital Gains Account Scheme (CGAS) is available in Section 54, 54B, 54D, 54EE, 54F, 54G, 54GA.

When Capital Asset is compulsorily acquired under any law, then the time limit for investment in new asset or making deposit in CGAS will be computed from the receipt of compensation.

Deduction u/s 54F and 54 is available in case new residential house property bought in the name of spouse.

If loan taken against the bonds or units specified by CG under section 54EC or 54EE, shall be deemed as conversion and to be charged to tax in the year of transfer.

Additional conditions for Section 54F :

On the date of original transfer, assessee to not own more than 1 house.

Should not purchase / construct any other house within 2 years / 3 years after the date of transfer.

Maximizing Benefits and Common Pitfalls to Avoid

There are common pitfalls that taxpayers must avoid to ensure their claims are valid. Missing deadlines is one of the most frequent mistakes, resulting in disqualification from deductions. For instance, failing to reinvest capital gains proceeds within the specified period can nullify the benefits. Similarly, not meeting investment requirements—such as not investing the full amount of capital gains or purchasing non-qualifying assets—can lead to a disallowance of deductions. Misinterpreting the applicability of specific sub-sections, like confusing the requirements of Section 54 with Section 54F, can also result in non-compliance.

Consider the hypothetical case of Ramesh, who sold his ancestral property and reinvested the gains in a residential property. However, Ramesh missed the deadline for this reinvestment by a few days. Consequently, he was unable to claim the deduction under Section 54, substantially increasing his tax liability. Likewise, another taxpayer, Priya, inaccurately documented her investment in bonds, only realizing her mistake during an audit, which led to her deduction being disallowed.

To minimize the risk of such pitfalls, taxpayers should regularly review and update their documentation, adhere to investment timelines, and consult tax professionals for clarity on the legal provisions. These steps ensure compliance with tax laws, ultimately aiding in the effective utilization of capital gains tax deductions.

Let's conquer the world of Taxes together, one step at a time! You can reach out to the Numbreylla Team for any assistance.

Overview of Capital Gains and Tax Deductions

Are you looking for ways to reduce your tax liability?

If so, you may be able to take advantage of the capital gains tax deductions available under the Income Tax Act. Budget 2024 has brought some serious changes for Capital Gain Taxes ranging from holding periods and tax rates to indexation benefits removal, and now, reintroduction as an option.

Capital gains represent the profit earned from the sale of an asset, such as real estate, stocks, or bonds, when the selling price exceeds the purchase price. These gains are classified into two categories: short-term capital gains (STCG) and long-term capital gains (LTCG), each subject to different tax treatments under Indian tax laws.

Short-term capital gains arise when an asset is held for a brief period—typically less than 12 or 24 months (36 months holding period now removed). These gains are typically taxed at a higher rate than the Long-term capital gains.

Tax deductions and exemptions play a crucial role in the financial planning of individuals and investors. These mechanisms are instituted to incentivize particular types of investments or economic activities, thereby promoting growth and financial stability. For instance, Section 80C offers deductions on specific investment instruments, while Section 10 offers exemptions on certain types of incomes.

Among the most significant provisions for tax relief on capital gains are Sections 54 and its related sections of the Income Tax Act. These sections primarily address exemptions on long-term capital gains, particularly from the sale of residential property, provided the gain is reinvested in specified assets, such as another residential property. This legal framework not only helps taxpayers significantly reduce their overall tax liability but also encourages the reinvestment of gains into the real estate market, bolstering economic activity within this sector.

Detailed Explanation of Section 54 and Its related sections

Section 54 and its related sections of the Income Tax Act provides avenues for taxpayers in India to reduce their capital gain tax liability through reinvestment. Here is a comprehensive breakdown of all those provisions, designed for easy understanding.

Section 54

Section 54B

Section 54D

Section 54EC

Section 54EE

Section 54F

Section 54G

Section 54GA

Some Points to note :

Capital Gains Account Scheme (CGAS) is available in Section 54, 54B, 54D, 54EE, 54F, 54G, 54GA.

When Capital Asset is compulsorily acquired under any law, then the time limit for investment in new asset or making deposit in CGAS will be computed from the receipt of compensation.

Deduction u/s 54F and 54 is available in case new residential house property bought in the name of spouse.

If loan taken against the bonds or units specified by CG under section 54EC or 54EE, shall be deemed as conversion and to be charged to tax in the year of transfer.

Additional conditions for Section 54F :

On the date of original transfer, assessee to not own more than 1 house.

Should not purchase / construct any other house within 2 years / 3 years after the date of transfer.

Maximizing Benefits and Common Pitfalls to Avoid

There are common pitfalls that taxpayers must avoid to ensure their claims are valid. Missing deadlines is one of the most frequent mistakes, resulting in disqualification from deductions. For instance, failing to reinvest capital gains proceeds within the specified period can nullify the benefits. Similarly, not meeting investment requirements—such as not investing the full amount of capital gains or purchasing non-qualifying assets—can lead to a disallowance of deductions. Misinterpreting the applicability of specific sub-sections, like confusing the requirements of Section 54 with Section 54F, can also result in non-compliance.

Consider the hypothetical case of Ramesh, who sold his ancestral property and reinvested the gains in a residential property. However, Ramesh missed the deadline for this reinvestment by a few days. Consequently, he was unable to claim the deduction under Section 54, substantially increasing his tax liability. Likewise, another taxpayer, Priya, inaccurately documented her investment in bonds, only realizing her mistake during an audit, which led to her deduction being disallowed.

To minimize the risk of such pitfalls, taxpayers should regularly review and update their documentation, adhere to investment timelines, and consult tax professionals for clarity on the legal provisions. These steps ensure compliance with tax laws, ultimately aiding in the effective utilization of capital gains tax deductions.

Let's conquer the world of Taxes together, one step at a time! You can reach out to the Numbreylla Team for any assistance.